Back To Blogs

Latest Advice

The Next Phase of the Streaming Wars

By Prime Talent Solutions

5 min read

Why Distribution Is Becoming More Valuable Than Content

For more than a decade, the streaming industry believed content was the ultimate competitive advantage.

FOX already owns sports rights, news programming, entertainment assets, and Tubi.

Yet it just agreed to spend approximately $22 billion acquiring a company that produces almost no original content of its own.

The question is obvious. If content remains king, why are some of the industry’s largest strategic bets increasingly being placed elsewhere?

The companies exerting the greatest influence over audience behaviour are often those controlling discovery, recommendation, operating systems, advertising infrastructure, audience intelligence, and platform access. In other words: not the people making the shows, but the people standing between the audience and the shows.

That is the shift FOX’s acquisition of Roku puts on full display.

The streaming wars are not ending because content no longer matters. They are entering a new phase because content is no longer the sole battleground.

The Deal

On June 15, 2026, FOX Corporation announced a definitive agreement to acquire Roku in a cash-and-stock transaction valuing the company at approximately $22 billion in enterprise value, expected to close in the first half of 2027. What FOX is buying is not a content library, it’s Roku’s connected TV operating system, The Roku Channel, its advertising infrastructure, its first-party audience data, and its direct relationship with more than 100 million streaming households worldwide. Paired with FOX’s own content slate and its free streaming service, Tubi, the combined company controls both a meaningful content footprint and the operating layer millions of households use to find something to watch.

That position, sitting at the exact point where consumers decide what to watch, is leverage. And leverage is where value has historically accumulated across technology markets.

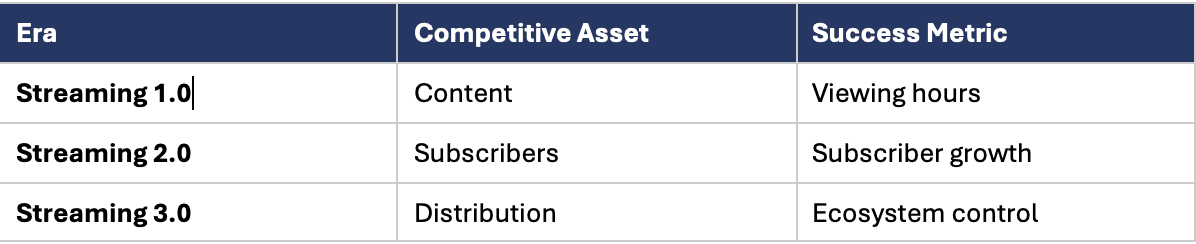

Three Eras of Streaming

For more than a decade, streaming competition centred on a relatively simple objective: build the strongest content library, attract the largest subscriber base, and create enough scale to justify ongoing investment. That model produced the first generation of streaming winners, Netflix investing heavily in originals, Disney consolidating premium franchises, Warner Bros. Discovery expanding its content portfolio, Amazon integrating entertainment into a broader consumer ecosystem.

The industry has quietly moved through three distinct competitive eras since:

Each era didn’t replace the last so much as raise the bar. Content is still necessary. It is no longer sufficient. The companies exerting the greatest influence over audience behaviour today are the ones controlling discovery, recommendation, operating systems, advertising infrastructure, audience intelligence, and platform access; the layer that sits between the content and the viewer.

In Streaming 3.0, controlling discovery may become more valuable than creating content. The next generation of winners may be determined less by what audiences watch and more by who controls what audiences see first.

This is not an argument that content no longer matters. Content remains the fuel that powers every streaming ecosystem; without it, there is nothing to distribute. The question is whether content alone remains sufficient to create durable competitive advantage. Increasingly, the evidence suggests it does not. Netflix’s library still drives engagement, but some of the most consequential strategic moves in the industry are increasingly occurring around the distribution layer rather than the content layer.

The macro numbers support the timing. Connected TV ad spend is on track to reach roughly $38 billion in the US in 2026, up around 14-15% year-on-year, while linear TV spend is projected to decline by more than 11% over the same period. For the first time, US CTV upfront commitments ($17.73 billion) are expected to exceed primetime linear upfront spending ($16.98 billion). The money is following the same path as the strategy: toward the platforms that sit closest to the viewer’s remote.

A Familiar Pattern

The implications extend far beyond one acquisition. Across technology markets, competitive advantage increasingly sits between producers and consumers rather than exclusively with either group. Google controls discovery. Apple controls access. Amazon controls commerce. YouTube controls creator distribution. The most powerful platforms increasingly own the interface rather than the product itself. Streaming appears to be following the same path, and the FOX-Roku deal is the clearest evidence yet.

What Leaders Should Watch Next

This transition carries real consequences for strategic planning, investment priorities, organisational design, and talent acquisition. Companies competing primarily as content businesses may find themselves at a structural disadvantage against organisations that control distribution, measurement, advertising infrastructure, recommendation engines, and audience relationships.

A handful of signals are worth tracking over the next 12-18 months:

More consolidation between content owners and distribution platforms, following the FOX-Roku template.

Greater focus on audience identity and measurement, as first-party data becomes the currency that justifies premium advertising rates.

Rising demand for platform, advertising, and data engineering talent, as distribution infrastructure becomes a board-level priority rather than a back-office function.

More competition for control of the home screen, as the operating layer between viewer and content becomes as valuable as the content itself.

The result is a market increasingly shifting from content economics toward distribution economics. The FOX-Roku deal alone will not create that future. It simply provides one of the clearest signals yet that it is already arriving.

The Talent Implication

If Streaming 3.0 is defined by ecosystem control rather than content ownership, demand will increasingly concentrate around recommendation engineers, advertising infrastructure specialists, audience measurement experts, platform product leaders, identity architects, and operating system talent.

These are not roles that traditional content-first organisations have historically prioritised in their hiring strategies, and many compensation and capability frameworks have not yet caught up to their value.

As distribution becomes a greater source of competitive advantage, the organisations that can attract, retain, and develop these capabilities are likely to gain advantages not only in market position, but in talent acquisition itself.

Prediction: Within five years, audience ownership, operating systems, advertising infrastructure, and first-party data will be valued more highly than incremental content libraries.

Sources: FOX Corporation press release (foxcorporation.com); Roku Form 425 SEC filing; CNBC; eMarketer CTV/linear ad spend forecasts, 2026.